Published August 26, 2011

Household debt burden exceeds that of US before sub-prime crisis

(SEOUL) If thrift is an Asian virtue, then it is one that South Koreans are notably lacking: each adult has almost five credit cards on average and the household debt burden exceeds that of the United States before the sub-prime crisis.

With the growing risk of a global double-dip recession hitting exports from Asia's fourth largest economy, consumer spending has been key to economic growth.

But household borrowing has propped up that spending. With debt far above levels that triggered a credit-card crisis eight years ago, it is now perhaps the biggest risk that Korea faces and one that the government is loath to tackle ahead of elections next year.

Alongside the mainstream banks, there has been robust growth from kerb market lenders. One even advertises that it will transfer funds after an 11-second procedure on a smartphone.

Official data shows that loans from these secondary lenders grew almost 10 per cent in 2010 to 7.5 trillion won (S$8.3 billion) as they tapped into insatiable demand from students, housewives and office workers.

Household debt 'is really serious and getting more so day by day', said Hong Hee-deok, a lawmaker with the opposition Democratic Labor Party. 'Many people now have to borrow more to pay interest, and those who can't see their debt principle snowballing each day. If not dealt with quickly, I think this could cause troubles that may lead to another sovereign crisis,' he warned.

Private economists are not that worried. True, any talk of the high consumer indebtedness is a blast from the past for those familiar with the 2003 credit card crisis in which millions defaulted and the central bank was compelled to inject funds into a tense bond market.

But it is premature to anticipate a 2003-like endgame, said Frederic Neumann, co-head of Asian Economics Research at HSBC in Hong Kong. 'Should household debt growth remain high for a long time, this would inevitably raise risks for financial stability. But, for the time being, this is not on the horizon.'

Korean household debt reached 155 per cent of disposable income in 2010, exceeding the 138 per cent recorded in the US at the outset of the sub-prime crisis, said Erik Lueth, an economist at Royal Bank of Scotland in Hong Kong.

For some Koreans, the debt burden has already become unsustainable. Kim, a shoe polisher working in central Seoul who declined to give his first name, said credit troubles contributed to the failure of his marriage and he was struggling to pay off his debts.

'One of my customers from Chohung Bank one day told me I can get a card easily and indeed came back later with a gold card issued for me. It was all because of the card that my life has collapsed thereafter,' he explained.

South Korea has been bitten by debt before. In 1997, heavy company borrowing triggered a near sovereign insolvency, but companies have cut debts close to 100 per cent of equity from 425 per cent at that time. The government also has strong finances.

Concerns that another global recession will hit exporters hard may also be overblown. Exports to the most vulnerable economies, the US and Europe, have fallen to 25 per cent of the total from nearly 40 per cent in 1997 as Korean companies have tapped into fast-growing markets like China.

That leaves household debt as the biggest risk and, so far, government action has been muted.

It says the bulk of household debts are owed by rich people and relatively well covered with collateral, and points out that loans from banks or conventional financial institutions are relatively sound, with delinquency ratios staying below one per cent for banks and below 2 per cent for credit card loans.

In June, it asked lenders to cap overall lending growth below the nominal economic growth rate of around 7-8 per cent annually, in addition to an earlier policy of limiting lending growth to below deposit growth.

'The measures were not aimed at reducing the total amount of loans, but I think they were the best option available to the government to curb debt growth while minimising the impact on economic growth,' said Lee Sang-jae, chief economist at Hyundai Securities in Seoul.

Indeed, the heavy debt servicing burden at households has become the single biggest factor affecting economic and financial policymaking in South Korea.

The Bank of Korea's reluctance to raise rates lock-step with rising inflation seems to be directly related to the debt situation, either for fear it may trigger a wave of defaults or that it will rein in spending. A percentage point increase in interest rates could, in theory, take about US$8 billion off Korean private consumption.

While Korea has won plaudits for its response to surging global capital flows and its leadership role in the Group of 20 nations' response to the fallout from the US credit crisis, it appears to have forgotten lessons from financial meltdowns.

In the wake of the 1997-1998 Asian financial crisis, Seoul encouraged banks to issue as many credit cards as possible so as to boost consumer spending, and by 2002 the number of cards in circulation surged 2.7 times to 105 million.

By the time the inevitable crisis came, Koreans had an average 4.6 cards per adult and a whopping US$100 billion in debt on them. The average ratio of debt to disposable income for households hit 108 per cent in 2002, right before the credit-card crisis broke out. Millions of defaults ensued and the government was forced to step in and bail out the country's then largest issuer, LG Card.

Card-ownership levels dropped to as low as 3.5 per adult in 2005, but have surged again to stand at nearly five per adult at the end of March this year, according to official data, as Koreans use them to pay for everything from coffee to luxury cars. -- Reuters

Friday, August 26, 2011

Advice for newly-formed households

26 August 2011

Colin Tan

In a weekend feature article, prospective buyers of homes - both for own occupation and for investment - got a huge dose of advice from property experts, consultants and even developers. Much of the advice was not new but there were many good reminders amid the volatile and uncertain economic environment - both locally and globally.

However, the needs of newly-formed households were not addressed as most had assumed that the majority in this group do not really have a choice but to apply for new public housing flats.

But in case you are one of those new households in a dilemma as to what you should do because you have a choice, I would say: Go for new public housing flats if you qualify, even if you can afford better. After all, it is every citizen's entitlement to subsidised housing. Why buy a private unit that is not subsidised?

And unless your housing needs leave you with no choice, avoid buying HDB resale flats as prices today are determined by a very unusual set of market circumstances - a combination of a severe supply crunch and a wayward price spiral in the private housing market. With sounder housing policies being put in place, such a scenario would not likely happen again for a very long time.

For all households, affordability should be a top concern. You do not want to spend your whole life working to pay off your mortgage or have your chances of upgrading minimised. Remember, HDB resale flat prices are at their highest now. Yes, they may continue to rise for a bit more due to the current supply crunch - but what after that?

Also in my opinion, the current prices are unsustainable. The majority of new households just cannot afford them, which is why the HDB is selling a lot more new flats - 25,000 units this year and another 25,000 in the next. Leave the market to those who do not have a choice. The premium factor for resale flats today may also negate whatever CPF housing grant you may be receiving.

With the recent raising of the household income ceiling to S$12,000 per month for Executive Condominium (EC) units, more households now qualify for them. If you are one of those thinking of EC apartments as your first buy, do remember that the units are priced to achieve a profit and at a level that the market can bear. Under the current market conditions, who do you think has the upper hand? Moreover, you are competing with the sandwiched class who have no choice but to apply for ECs.

If you are thinking of the investment potential of your first buy and you want to buy something other than new HDB flats, you would be wise to set this thought aside in the current economic environment. It is already difficult to arrive at a "correct" choice in a stable market, what more when the present environment is in such a turmoil.

Nobody can predict the future. When you consider the investment potential of a purchase, you are actually gambling. You are taking a position on the market - that it will continue to rise in the future. It was less of a gamble in the past as Singapore - or the world for that matter - was a lot less complex than it is today.

Most new households are not sophisticated in that they do not follow the developments in the housing market closely. But those who do may be worried about the oversupply of HDB resale flats some seven to eight years down the road. This is because the 50,000 HDB flats sold this year and the next will mature then. Will resale prices be depressed then?

Anything can happen between now and then to drastically alter the market scenario. Nevertheless, with more selling their units, you can expect prices to be softer. And if there is no support from HDB upgraders, mass market private prices will have to come down to link the two markets again.

If you think about it, it is not really a negative situation to sell low and buy low when upgrading. In fact, it is the ideal situation. The loan quantum needed is actually smaller to sell lower and buy lower by, say 10 per cent, than to sell higher and buy higher by 10 per cent. Work it out yourself.

The writer is head of research & consultancy at Chesterton Suntec International.

Colin Tan

In a weekend feature article, prospective buyers of homes - both for own occupation and for investment - got a huge dose of advice from property experts, consultants and even developers. Much of the advice was not new but there were many good reminders amid the volatile and uncertain economic environment - both locally and globally.

However, the needs of newly-formed households were not addressed as most had assumed that the majority in this group do not really have a choice but to apply for new public housing flats.

But in case you are one of those new households in a dilemma as to what you should do because you have a choice, I would say: Go for new public housing flats if you qualify, even if you can afford better. After all, it is every citizen's entitlement to subsidised housing. Why buy a private unit that is not subsidised?

And unless your housing needs leave you with no choice, avoid buying HDB resale flats as prices today are determined by a very unusual set of market circumstances - a combination of a severe supply crunch and a wayward price spiral in the private housing market. With sounder housing policies being put in place, such a scenario would not likely happen again for a very long time.

For all households, affordability should be a top concern. You do not want to spend your whole life working to pay off your mortgage or have your chances of upgrading minimised. Remember, HDB resale flat prices are at their highest now. Yes, they may continue to rise for a bit more due to the current supply crunch - but what after that?

Also in my opinion, the current prices are unsustainable. The majority of new households just cannot afford them, which is why the HDB is selling a lot more new flats - 25,000 units this year and another 25,000 in the next. Leave the market to those who do not have a choice. The premium factor for resale flats today may also negate whatever CPF housing grant you may be receiving.

With the recent raising of the household income ceiling to S$12,000 per month for Executive Condominium (EC) units, more households now qualify for them. If you are one of those thinking of EC apartments as your first buy, do remember that the units are priced to achieve a profit and at a level that the market can bear. Under the current market conditions, who do you think has the upper hand? Moreover, you are competing with the sandwiched class who have no choice but to apply for ECs.

If you are thinking of the investment potential of your first buy and you want to buy something other than new HDB flats, you would be wise to set this thought aside in the current economic environment. It is already difficult to arrive at a "correct" choice in a stable market, what more when the present environment is in such a turmoil.

Nobody can predict the future. When you consider the investment potential of a purchase, you are actually gambling. You are taking a position on the market - that it will continue to rise in the future. It was less of a gamble in the past as Singapore - or the world for that matter - was a lot less complex than it is today.

Most new households are not sophisticated in that they do not follow the developments in the housing market closely. But those who do may be worried about the oversupply of HDB resale flats some seven to eight years down the road. This is because the 50,000 HDB flats sold this year and the next will mature then. Will resale prices be depressed then?

Anything can happen between now and then to drastically alter the market scenario. Nevertheless, with more selling their units, you can expect prices to be softer. And if there is no support from HDB upgraders, mass market private prices will have to come down to link the two markets again.

If you think about it, it is not really a negative situation to sell low and buy low when upgrading. In fact, it is the ideal situation. The loan quantum needed is actually smaller to sell lower and buy lower by, say 10 per cent, than to sell higher and buy higher by 10 per cent. Work it out yourself.

The writer is head of research & consultancy at Chesterton Suntec International.

History does not repeat itself but it does rhyme

26 August 2011

Tan Chin Keong

The Singapore residential property market has recently exhibited pricing anomalies that remind us of the conditions prevalent during the last market peak in 2007. Back then, exuberant market conditions as well as their own ingenuity allowed property developers to sell some large luxury residential units at a higher price per sq ft (psf) than the smaller units in the same project.

This time, history did not repeat itself but what we have now sure sounds like a rhyme.

In October 2007, a 5,048 sq ft penthouse unit at Orchard Residences sold for a then-record price of S$5,600 per sq ft - significantly higher than the project's average price of around S$3,300 psf based on caveats lodged by purchasers. Other developers held auctions for their penthouse units in hopes of achieving a higher per-square-foot selling price - and they largely succeeded.

That was a pricing anomaly, as small units are normally sold at a higher price per sq ft than larger units (similar to retail versus bulk prices in consumer items). In hindsight, this anomaly turned out to be a warning sign indicating the market's over-exuberance, as residential property prices subsequently fell by an average of 25 per cent in 2008 and the first half of 2009.

Fast-forward four years to today - we are now facing a different form of pricing anomaly.

With the rising popularity of small "shoebox" units as I highlighted in this column last month ("Shoebox trend a boon for developers and retailers," July 15), the pricing pendulum seems to have swung to the other extreme.

Based on caveats lodged on some recent residential property launches, shoebox units are currently selling at a large price-per-sq-ft premium of 30 to 80 per cent over three- to four-room units in the same project.

For example, The Lakefront Residences, a popular project launched in the Jurong Lakeside precinct late last year, saw its small units sold at around 80 per cent price premium to the larger units. According to the caveats on the project, shoebox units of less than 600 sq ft sold at an average of around S$1,300 psf, well above the average S$700 psf price for the larger units with floor space of more than 1,500 sq ft.

While I have said that smaller units should be sold at a higher price per sq ft, a premium of around 80 per cent does seem like an anomaly to me.

A hint of things to come?

Other than this pricing anomaly, another interesting - and potentially foreboding - trend worth highlighting is that in past years, every time the Government introduced significant measures to cool residential property prices, it was followed the next year by an external crisis that triggered a sharp correction in prices.

For example, in May 1996, the Government introduced a capital gains tax to curb residential property price increases. This was followed by the Asian financial crisis in 1997, which triggered a sharp price decline in the market from 1997 to 1998.

Another example is in October 2007, when the Government introduced measures to stop deferred-payment schemes in the residential market. Again, this was followed by an external crisis - the US subprime fiasco of 2008 - that triggered another tumble in the local market. Singapore's residential prices (mainly private properties, as public HDB flat prices held relatively steady due to supply shortage) fell an average of 25 per cent in 2008 and the first half of 2009.

By now, readers will have sensed the uncanny resemblance between the current conditions and those of 1996 and 2007. Over the last 12 months, the Government has introduced a number of harsh measures to cool the residential property market - including sharply higher seller's stamp duties and lower loan-to-value ratios for mortgages - while global macroeconomic conditions have turned increasingly uncertain, especially over the last few weeks.

In addition, the pricing anomaly that we are currently seeing in the form of the huge price premiums commanded by shoebox units also reminds us the over-exuberance we saw in 2007.

However, it is also not all bad news as the uncertain macroeconomic conditions would mean that low interest rates, which have been supportive of residential property prices so far, would stay for a prolonged period.

But if the quote "History doesn't repeat itself, but it does rhyme," is to be believed, then Singapore's residential property market may not be singing as sweet a tune as before.

Tan Chin Keong is an analyst at UBS Wealth Management Research.

Tan Chin Keong

The Singapore residential property market has recently exhibited pricing anomalies that remind us of the conditions prevalent during the last market peak in 2007. Back then, exuberant market conditions as well as their own ingenuity allowed property developers to sell some large luxury residential units at a higher price per sq ft (psf) than the smaller units in the same project.

This time, history did not repeat itself but what we have now sure sounds like a rhyme.

In October 2007, a 5,048 sq ft penthouse unit at Orchard Residences sold for a then-record price of S$5,600 per sq ft - significantly higher than the project's average price of around S$3,300 psf based on caveats lodged by purchasers. Other developers held auctions for their penthouse units in hopes of achieving a higher per-square-foot selling price - and they largely succeeded.

That was a pricing anomaly, as small units are normally sold at a higher price per sq ft than larger units (similar to retail versus bulk prices in consumer items). In hindsight, this anomaly turned out to be a warning sign indicating the market's over-exuberance, as residential property prices subsequently fell by an average of 25 per cent in 2008 and the first half of 2009.

Fast-forward four years to today - we are now facing a different form of pricing anomaly.

With the rising popularity of small "shoebox" units as I highlighted in this column last month ("Shoebox trend a boon for developers and retailers," July 15), the pricing pendulum seems to have swung to the other extreme.

Based on caveats lodged on some recent residential property launches, shoebox units are currently selling at a large price-per-sq-ft premium of 30 to 80 per cent over three- to four-room units in the same project.

For example, The Lakefront Residences, a popular project launched in the Jurong Lakeside precinct late last year, saw its small units sold at around 80 per cent price premium to the larger units. According to the caveats on the project, shoebox units of less than 600 sq ft sold at an average of around S$1,300 psf, well above the average S$700 psf price for the larger units with floor space of more than 1,500 sq ft.

While I have said that smaller units should be sold at a higher price per sq ft, a premium of around 80 per cent does seem like an anomaly to me.

A hint of things to come?

Other than this pricing anomaly, another interesting - and potentially foreboding - trend worth highlighting is that in past years, every time the Government introduced significant measures to cool residential property prices, it was followed the next year by an external crisis that triggered a sharp correction in prices.

For example, in May 1996, the Government introduced a capital gains tax to curb residential property price increases. This was followed by the Asian financial crisis in 1997, which triggered a sharp price decline in the market from 1997 to 1998.

Another example is in October 2007, when the Government introduced measures to stop deferred-payment schemes in the residential market. Again, this was followed by an external crisis - the US subprime fiasco of 2008 - that triggered another tumble in the local market. Singapore's residential prices (mainly private properties, as public HDB flat prices held relatively steady due to supply shortage) fell an average of 25 per cent in 2008 and the first half of 2009.

By now, readers will have sensed the uncanny resemblance between the current conditions and those of 1996 and 2007. Over the last 12 months, the Government has introduced a number of harsh measures to cool the residential property market - including sharply higher seller's stamp duties and lower loan-to-value ratios for mortgages - while global macroeconomic conditions have turned increasingly uncertain, especially over the last few weeks.

In addition, the pricing anomaly that we are currently seeing in the form of the huge price premiums commanded by shoebox units also reminds us the over-exuberance we saw in 2007.

However, it is also not all bad news as the uncertain macroeconomic conditions would mean that low interest rates, which have been supportive of residential property prices so far, would stay for a prolonged period.

But if the quote "History doesn't repeat itself, but it does rhyme," is to be believed, then Singapore's residential property market may not be singing as sweet a tune as before.

Tan Chin Keong is an analyst at UBS Wealth Management Research.

Wednesday, August 24, 2011

'Standard' models can't explain crashes

Published August 24, 2011

Professor presents mathematical model for 'jumps', advises investors to decide on investment policy before any crisis, reports GENEVIEVE CUA

AS grave uncertainties roil markets, some in the academe are working to model financial crises and the domino effect that can ensue, as a shock in one major market sparks off turmoil in other markets and assets.

Yacine Ait-Sahalia, director of Bendheim Centre for Finance at Princeton University, presented a mathematical model for 'jumps', a deceptively innocuous term for market shocks or sudden downdrafts such as has been seen in recent weeks and years.

The big question is - how should portfolios be optimised with a view to such shocks?

Speaking to an audience of investment managers this week, Professor Yacine says there is no mechanism in the classical formula to account for sudden market moves. 'We tend to optimise portfolios well for good times when we don't need it, but not for bad times when optimisation will be helpful.'

Prof Yacine is also the Otto A. Hack 1903 Professor of Finance and Economics. He was the guest speaker at a lunch this week, jointly organised by the Centre for Asset Management Research & Investments and the Investment Management Association of Singapore.

'Rebalancing a portfolio is a disciplined way of fighting the worst behavioural instincts which lead you to make major investment mistakes.'

- Prof Yacine

Classical finance assumes a rational market where risk-averse investors allocate assets broadly between a market portfolio and cash, with a view to maximising returns at a given level of risk.

Any number of factors can derail that smoothly functioning assumption, however, as recent years have painfully shown. In a crisis, asset correlations converge, for instance, which means that most risk assets rise and fall together. Investors cease to be rational and turn risk averse at the worst time, selling down assets that have already been beaten down and exacerbating the plunge. All these mean that diversification, which is supposed to shield portfolios from the worst of losses, may well fail at extreme moments.

Prof Yacine's presentation touched on the nature of crises, where a shock in one market appears to raise the probabilility of successive shocks not only in the affected asset class, but also in other asset classes. These crashes, he says, cannot be explained by 'standard' models which tend to see market shocks as discrete and independent events.

Examples of the contagion effect of shocks include the crash in October 2008 where over a space of five trading sessions, the US market dropped 35 per cent, and sparked a slide as well in the Pacific and European markets. The current downturn is yet another instance.

About October 2008, he says: 'This (price fall) was a move you might have expected to see once every few years on average. . . But to have a move like this every day for five days in a row, an event like this (is) very, very unusual - almost impossible under any of the standard models.'

To capture the possible contagion effect of market shocks, Prof Yacine uses a model called 'Hawkes processes', originally used to model epidemics. Under this model, a shock in one region of the world or segment of the market raises the intensity of jumps or shocks occurring, before things eventually 'mean revert' or return to some long-term average level.

What should investors do? There are some who believe that in the long term, asset prices will settle to a long-term average and time will smooth out short-term volatility. The rub of this thinking is that in a vicious downdraft where most asset prices plunge, you could well lose most of your savings, making recovery difficult.

Prof Yacine proposes that instead of classical theory's two-asset portfolio, investors should have basically three assets - an asset that is a long position on market risk; a long/short fund which hedges against 'jump risks', and cash or the money market.

He told reporters after the presentation that investors should basically hold assets that benefit from a flight to quality. These include US Treasuries, yen assets, German bund and gold. Today, a diversified portfolio may already include a modest allocation to gold, and certainly some to bonds.

At times of crisis, investors should rebalance their portfolio, buying more of the hedges against so-called jump risk.

He said: 'Once you see a jump or turbulent times, you need to rebalance, with anticipation that there will be more jumps and that they're not isolated.

'Rebalancing a portfolio is a disciplined way of fighting the worst behavioural instincts which lead you to make major investment mistakes. . . If you force yourself to rebalance, that leads you to buy more of what has dropped in value and sell what has gone up.'

The catch is that investors should decide on their investment policy before any crisis, and stick to it, rather than formulate a policy on the fly. 'It's very difficult to invent yourself a rebalancing policy in the middle of a crisis. You need to have a policy you are comfortable with in good times and are committed to sticking to. That's the key; you need to (do) it automatically. If you think about it, you give a chance for behavioural factors to come into play.'

Another catch is that picking up the 'jump hedges' such as gold or US Treasuries when a crisis hits means you are likely to be buying when prices of those assets have already risen. Gold, for instance, yesterday briefly crossed a record US$1,900 an ounce.

'If you weren't properly hedged at the first jump, you get a chance to re-hedge. Clearly it will be costly to rebalance. The first jump will change the prices of assets, but that's life - there is no free lunch,' Prof Yacine says.

Professor presents mathematical model for 'jumps', advises investors to decide on investment policy before any crisis, reports GENEVIEVE CUA

AS grave uncertainties roil markets, some in the academe are working to model financial crises and the domino effect that can ensue, as a shock in one major market sparks off turmoil in other markets and assets.

Yacine Ait-Sahalia, director of Bendheim Centre for Finance at Princeton University, presented a mathematical model for 'jumps', a deceptively innocuous term for market shocks or sudden downdrafts such as has been seen in recent weeks and years.

The big question is - how should portfolios be optimised with a view to such shocks?

Speaking to an audience of investment managers this week, Professor Yacine says there is no mechanism in the classical formula to account for sudden market moves. 'We tend to optimise portfolios well for good times when we don't need it, but not for bad times when optimisation will be helpful.'

Prof Yacine is also the Otto A. Hack 1903 Professor of Finance and Economics. He was the guest speaker at a lunch this week, jointly organised by the Centre for Asset Management Research & Investments and the Investment Management Association of Singapore.

'Rebalancing a portfolio is a disciplined way of fighting the worst behavioural instincts which lead you to make major investment mistakes.'

- Prof Yacine

Classical finance assumes a rational market where risk-averse investors allocate assets broadly between a market portfolio and cash, with a view to maximising returns at a given level of risk.

Any number of factors can derail that smoothly functioning assumption, however, as recent years have painfully shown. In a crisis, asset correlations converge, for instance, which means that most risk assets rise and fall together. Investors cease to be rational and turn risk averse at the worst time, selling down assets that have already been beaten down and exacerbating the plunge. All these mean that diversification, which is supposed to shield portfolios from the worst of losses, may well fail at extreme moments.

Prof Yacine's presentation touched on the nature of crises, where a shock in one market appears to raise the probabilility of successive shocks not only in the affected asset class, but also in other asset classes. These crashes, he says, cannot be explained by 'standard' models which tend to see market shocks as discrete and independent events.

Examples of the contagion effect of shocks include the crash in October 2008 where over a space of five trading sessions, the US market dropped 35 per cent, and sparked a slide as well in the Pacific and European markets. The current downturn is yet another instance.

About October 2008, he says: 'This (price fall) was a move you might have expected to see once every few years on average. . . But to have a move like this every day for five days in a row, an event like this (is) very, very unusual - almost impossible under any of the standard models.'

To capture the possible contagion effect of market shocks, Prof Yacine uses a model called 'Hawkes processes', originally used to model epidemics. Under this model, a shock in one region of the world or segment of the market raises the intensity of jumps or shocks occurring, before things eventually 'mean revert' or return to some long-term average level.

What should investors do? There are some who believe that in the long term, asset prices will settle to a long-term average and time will smooth out short-term volatility. The rub of this thinking is that in a vicious downdraft where most asset prices plunge, you could well lose most of your savings, making recovery difficult.

Prof Yacine proposes that instead of classical theory's two-asset portfolio, investors should have basically three assets - an asset that is a long position on market risk; a long/short fund which hedges against 'jump risks', and cash or the money market.

He told reporters after the presentation that investors should basically hold assets that benefit from a flight to quality. These include US Treasuries, yen assets, German bund and gold. Today, a diversified portfolio may already include a modest allocation to gold, and certainly some to bonds.

At times of crisis, investors should rebalance their portfolio, buying more of the hedges against so-called jump risk.

He said: 'Once you see a jump or turbulent times, you need to rebalance, with anticipation that there will be more jumps and that they're not isolated.

'Rebalancing a portfolio is a disciplined way of fighting the worst behavioural instincts which lead you to make major investment mistakes. . . If you force yourself to rebalance, that leads you to buy more of what has dropped in value and sell what has gone up.'

The catch is that investors should decide on their investment policy before any crisis, and stick to it, rather than formulate a policy on the fly. 'It's very difficult to invent yourself a rebalancing policy in the middle of a crisis. You need to have a policy you are comfortable with in good times and are committed to sticking to. That's the key; you need to (do) it automatically. If you think about it, you give a chance for behavioural factors to come into play.'

Another catch is that picking up the 'jump hedges' such as gold or US Treasuries when a crisis hits means you are likely to be buying when prices of those assets have already risen. Gold, for instance, yesterday briefly crossed a record US$1,900 an ounce.

'If you weren't properly hedged at the first jump, you get a chance to re-hedge. Clearly it will be costly to rebalance. The first jump will change the prices of assets, but that's life - there is no free lunch,' Prof Yacine says.

Gold prices will become 'parabolic', says economist

Published August 24, 2011

Analysts studying technical analysis tools say that bullion prices may be set to decline after record rally

(LONDON) Gold's rally to a record above US$1,900 an ounce has pushed the metal to overbought levels according to technical analysis tools, as economist Dennis Gartman said that prices will go 'parabolic'.

Still glittering: Demand for gold pushed holdings in ETPs to a record 2,216.8 tonnes on Aug 8, data compiled by Bloomberg show

Bullion's relative strength index has topped 70 since Aug 5, a signal to some investors who study technical charts that prices may be set to decline. Gold hugged its upper Bollinger band most of this month, which may signal possible resistance, while a moving average convergence/ divergence indicator and Elliot Wave patterns suggest that prices are overextended, said Ross Norman, chief executive officer of London bullion brokerage Sharps Pixley Ltd.

Gold futures climbed as high as US$1,904 an ounce in New York yesterday and is up 16 per cent in August, set for the best monthly gain since 1999. The metal has advanced as concern about debt crises and slower economic growth spurred investors to diversify holdings away from equities and some currencies. The biggest gold-backed exchange-traded product (ETP) surpassed its equities counterpart as the largest by market value, while bullion rose to record prices in euros, British pounds and Swiss francs.

'I think we're overextended in the short term,' Axel Rudolph, a technical strategist at Commerzbank AG here, said by phone. 'I wouldn't be surprised if we were to fail around US$1,900 to US$1,922, and retrace a little bit for a few days or so. It's still very bullish longer term. Longer term, I think US$2,000 will definitely be hit.'

Prices may slip to the Aug 11 high of about US$1,815 if gold stays below US$1,925, which is near a 60-minute point-and-figure target, Mr Rudolph said. The metal may move 'sideways to up' if no decline takes place in the next couple of days, he said.

Still, a weekly close above US$1,900 may push prices to the 'psychological' level of US$2,000, near the 200 per cent extension of the rally from January's low to May's high projected from the May low, one of the levels singled out in so-called Fibonacci analysis, he said. Fibonacci analysis is based on the theory that prices tend to drop or climb by certain percentages after reaching a high or low.

Gold futures for December delivery traded at US$1,901.90 at 5.15 pm on Comex in New York. In London, bullion for immediate delivery gained 2.5 per cent at 10.17 pm, after reaching US$1,900.60. It is up 34 per cent this year and heading for an 11th straight annual gain, the longest winning streak since at least 1920. The metal has outperformed global equities, commodities and Treasuries this year.

'Gold is strong in any and all currency terms, and it is now entering that stage when prices go parabolic,' Mr Gartman said yesterday. 'This will end when it ends; there is really nothing more that can or shall or should be said.'

Speculative demand from investors has pushed the gold market into a 'bubble that is poised to burst', Wells Fargo & Co said in an Aug 15 report. Prices may climb to US$2,000 an ounce by the end of the year, according to the median forecast in a Bloomberg survey of 13 traders and analysts at a conference in Kovalam in South India on Aug 20.

The precious metal's 'rally when by rights a period of consolidation or profit-taking would be expected suggests that gold is either simply not in technical 'mode' and that other external factors are driving us higher, or that we are in a panic phase which inevitably leads to a blow-off at the top', Sharps Pixley's Mr Norman said.

Demand for gold pushed holdings in ETPs to a record 2,216.8 tonnes on Aug 8, data compiled by Bloomberg show. Investors' assets in the products were 2,211.1 tonnes on Aug 19, more than all but four central banks. Central banks are also adding to gold reserves for the first time in a generation.

The market capitalisation of the SPDR Gold Trust, the biggest gold-backed ETP, rose to US$76.7 billion on Aug 19, according to the most recent data compiled by Bloomberg. SPDR S&P 500 ETF Trust, which had been the industry's largest ETP since 1993, was at US$74.4 billion.

Bullion's 14-day relative strength index (RSI), last at 83.61, reached 84.96 on Aug 10, the highest level since October, according to data compiled by Bloomberg. Prices fell as much as 7.3 per cent in the week after the gauge was at 84.61 on April 29 and traded in a US$115 range for the next two-and-a-half months.

'You can actually make forecasts, even if it's trading at new all-time highs,' Commerzbank's Mr Rudolph said. 'The problem with gold right now is that in the last three days, it's just accelerated higher - and when it's in this sort of move, it can still continue in fast spikes. It's very difficult to know where the spikes are going to end.' - Bloomberg

Analysts studying technical analysis tools say that bullion prices may be set to decline after record rally

(LONDON) Gold's rally to a record above US$1,900 an ounce has pushed the metal to overbought levels according to technical analysis tools, as economist Dennis Gartman said that prices will go 'parabolic'.

Still glittering: Demand for gold pushed holdings in ETPs to a record 2,216.8 tonnes on Aug 8, data compiled by Bloomberg show

Bullion's relative strength index has topped 70 since Aug 5, a signal to some investors who study technical charts that prices may be set to decline. Gold hugged its upper Bollinger band most of this month, which may signal possible resistance, while a moving average convergence/ divergence indicator and Elliot Wave patterns suggest that prices are overextended, said Ross Norman, chief executive officer of London bullion brokerage Sharps Pixley Ltd.

Gold futures climbed as high as US$1,904 an ounce in New York yesterday and is up 16 per cent in August, set for the best monthly gain since 1999. The metal has advanced as concern about debt crises and slower economic growth spurred investors to diversify holdings away from equities and some currencies. The biggest gold-backed exchange-traded product (ETP) surpassed its equities counterpart as the largest by market value, while bullion rose to record prices in euros, British pounds and Swiss francs.

'I think we're overextended in the short term,' Axel Rudolph, a technical strategist at Commerzbank AG here, said by phone. 'I wouldn't be surprised if we were to fail around US$1,900 to US$1,922, and retrace a little bit for a few days or so. It's still very bullish longer term. Longer term, I think US$2,000 will definitely be hit.'

Prices may slip to the Aug 11 high of about US$1,815 if gold stays below US$1,925, which is near a 60-minute point-and-figure target, Mr Rudolph said. The metal may move 'sideways to up' if no decline takes place in the next couple of days, he said.

Still, a weekly close above US$1,900 may push prices to the 'psychological' level of US$2,000, near the 200 per cent extension of the rally from January's low to May's high projected from the May low, one of the levels singled out in so-called Fibonacci analysis, he said. Fibonacci analysis is based on the theory that prices tend to drop or climb by certain percentages after reaching a high or low.

Gold futures for December delivery traded at US$1,901.90 at 5.15 pm on Comex in New York. In London, bullion for immediate delivery gained 2.5 per cent at 10.17 pm, after reaching US$1,900.60. It is up 34 per cent this year and heading for an 11th straight annual gain, the longest winning streak since at least 1920. The metal has outperformed global equities, commodities and Treasuries this year.

'Gold is strong in any and all currency terms, and it is now entering that stage when prices go parabolic,' Mr Gartman said yesterday. 'This will end when it ends; there is really nothing more that can or shall or should be said.'

Speculative demand from investors has pushed the gold market into a 'bubble that is poised to burst', Wells Fargo & Co said in an Aug 15 report. Prices may climb to US$2,000 an ounce by the end of the year, according to the median forecast in a Bloomberg survey of 13 traders and analysts at a conference in Kovalam in South India on Aug 20.

The precious metal's 'rally when by rights a period of consolidation or profit-taking would be expected suggests that gold is either simply not in technical 'mode' and that other external factors are driving us higher, or that we are in a panic phase which inevitably leads to a blow-off at the top', Sharps Pixley's Mr Norman said.

Demand for gold pushed holdings in ETPs to a record 2,216.8 tonnes on Aug 8, data compiled by Bloomberg show. Investors' assets in the products were 2,211.1 tonnes on Aug 19, more than all but four central banks. Central banks are also adding to gold reserves for the first time in a generation.

The market capitalisation of the SPDR Gold Trust, the biggest gold-backed ETP, rose to US$76.7 billion on Aug 19, according to the most recent data compiled by Bloomberg. SPDR S&P 500 ETF Trust, which had been the industry's largest ETP since 1993, was at US$74.4 billion.

Bullion's 14-day relative strength index (RSI), last at 83.61, reached 84.96 on Aug 10, the highest level since October, according to data compiled by Bloomberg. Prices fell as much as 7.3 per cent in the week after the gauge was at 84.61 on April 29 and traded in a US$115 range for the next two-and-a-half months.

'You can actually make forecasts, even if it's trading at new all-time highs,' Commerzbank's Mr Rudolph said. 'The problem with gold right now is that in the last three days, it's just accelerated higher - and when it's in this sort of move, it can still continue in fast spikes. It's very difficult to know where the spikes are going to end.' - Bloomberg

When blue chips give you the blues

Published August 24, 2011

MONEY MATTERS

Beware - while value-investing may seem easy, human frailty often turns it into 'unconscious speculation'

By WILLIAM CAI

IN THE third quarter of 2010, a slew of positive economic data was evident in the media. The idea of investing for the long term - by picking Singapore's 'solid' dividend-paying blue-chip stocks - became an attractive proposition in a low-interest-rate environment. Coincidentally, this was also when the Singapore Investor Confidence Index Poll reached a high. From a contrarian perspective, that's when one should worry.

A 'death cross' occurred when the Straits Times Index (STI) fell to 2,797. It's a term used when a security's 50-day moving average price line crosses over its 200-day moving average line from the top, generating a long-term bearish signal which suggests that investors should adjust their bullish view to bearish.

While 12 out of 18 'death crosses' resulted as false signals (whipsaws) over the past 30 years for the STI, investors should still take the bearish signal seriously. Firstly, as a lagging indicator, the signal usually occurs after the STI has fallen by 10 per cent or more, and only to be compounded by further losses if a severe bear emerges. Secondly, six out of the 18 signals resulted in losses ranging from minus 22 per cent to minus 54 per cent. Thirdly, it is worrying that more than 60 per cent of the STI constituents, which are classified as 'blue-chip' stocks, have generated the 'death cross' signal.

More importantly, the 'death cross' has also occurred for various other global markets, increasing the odds of a full-blown bear market.

The definition of an 'investment', as offered by Benjamin Graham in 1934, 'is an operation that promises the safety of principal and satisfaction of return. Operations not meeting these requirements are speculation.'

Contrary to popular belief, Warren Buffett is a great market timer. He plays the game well by raising cash when he cannot find attractively-valued stocks. He waits for opportunities to pick up stocks at fire-sale prices, especially when there's blood in the streets.

The biggest mistake an investor can make is to focus only on the idea of getting stable dividends, with disregard to price. For example, when investors buy blue chips at a high price during the mature stage of an economic cycle, this increases the possibility of seeing their stock value fall 50 per cent or more in the next economic slowdown.

Despite the potential poor risk-adjusted ratio, investors stick to the concept of buying blue-chip stocks as they harbour the hope of capital appreciation which bonds may not match. This does not make sense as corporate bonds can do the job of providing a steady income better without similar risk to equity.

Untrained investors would focus on buying blue chips with the highest reputation, quoting their good management and their ability to continue to deliver profits for the long term as reasons for investing in them. Such investors do not wish to engage in market-timing activities as they equate these to speculation. Therefore, they pay insufficient attention to prices given their assumption that well-chosen blue chips would recover from an economic downturn. Ironically, that is a speculative assumption as many of today's blue chips could become tomorrow's losers.

For example, an investor who bought SGX shares at $14.40 on Oct 2, 2007 would have seen the price fall 53 per cent as at Aug 22, 2011. Assuming dividends reinvested, the loss would be large at minus 46 per cent. Investors who bought stocks like Cosco, NOL and Yangzijiang at their peak in 2007 would still be nursing losses of between minus 50 per cent to minus 84 per cent.

Contrary to popular belief, Warren Buffett, the famous value investor, is a great market timer. He plays the game well by raising cash when he cannot find attractively-valued stocks. He waits for opportunities to pick up stocks at fire-sale prices, especially when there's blood in the streets. As the key to long-term investment success is to first avoid losing big, a true long-term investor should do the same and wait for a market crisis to buy stocks at attractive prices. Then, they can ignore the madness of short-term volatility and sell the stocks when they become overvalued. Over time, this strategy can substantially increase the wealth of investors.

For most investors, professionals included, qualitative factors like good management are difficult to deal with intelligently and such an evaluation can be clouded by an investor's own confirmation bias. Quantitative factors, like the continued ability for a business to deliver steady earnings growth, would need investors to have a considerable amount of investigation and business acumen.

Savvier investors could argue that Singapore stocks are now reasonable, based on their current price ratios and forward-looking evaluations. This requires the calculation of the intrinsic value of a business as determined by its future earnings. However, history has repeatedly shown that during the good times, many analysts become over-optimistic and assume a sustainable earnings trend. In reality, the concept of intrinsic value is arbitrary at best. It is elusive and hard to determine, due to the uncertain future and the irrational market.

In addition, few analysts dare to offer views different from the herd as it is often safer to err with the masses. For an analyst to be wrong alone, it can lead to the demise of his reputation and career. Even if the trend of earnings and intrinsic value can be determined reliably, it does not sufficiently provide a safe basis for investing, especially during a bear market.

Currently, the price-to-book (P/B) ratio for the STI stands at 1.3 times and history has also shown that since 1994, whenever the P/B ratio drops from 1.5 times, its downward momentum would bring it to lower levels. This assigns a high probability that the STI could have more to fall as it just breached its 1.5 times P/B level this month.

Unfortunately, during a mature economic cycle, undervalued blue chips are uncommon and many investors end up investing without sufficient regard to price. Investors should focus on value investing as it helps investors invest better by selecting stocks based on the margin-of-safety principle. This means that one buys undervalued stocks at a price lower than their intrinsic value.

This helps to prioritise the safety of capital while dividends are viewed as of secondary importance. While dividends come in handy as a 'cushion' to effectively lower losses when stock prices fall, dividend yields are lower when blue chips are bought at higher prices. Furthermore, during an economic downturn, companies do slash their dividend payouts to preserve cash holdings. This was true during the last crisis for blue chips like SIA, NOL, SGX, CapitaLand, DBS, UOB and ComfortDelgro, as their earnings fell.

While value-investing may seem easy, human frailty often prevents successful implementation. It is hard to prevent human emotion from corrupting an investment framework. Even if the necessary fundamental analysis is used to scan for value stocks, investors may end up with a handful of stocks from boring industries which are not what he initially deemed as blue chips. More importantly, it is hard to be fearful when others are greedy, and vice versa. It is hard to think independently and go against the herd.

Nevertheless, I hope that this article has helped instil a new level of consciousness to replace unconscious speculation. When the stock market enters a bear phase, extreme fear rather than fundamentals rules the day. Even the bluest of blue-chip value picks can fall by a considerable amount. Dividends are often insufficient to cushion a market bloodbath. How much more refuge can an expensive blue chip provide? Investors who buy stocks at a high premium during a stockmarket high unwittingly end up as 'long-term investors'.

With the current global economic slowdown, coupled with the lingering US and European sovereign debt crisis, the recent market carnage could be the beginning of something worse. Buying blue chips based on dividends alone while ignoring price, potentially deteriorating fundamentals and the economic cycle can be disastrous. It's never too late to avoid unconscious speculation and to invest wisely.

The writer is vice-president & deputy investment head at GYC Financial Advisory

MONEY MATTERS

Beware - while value-investing may seem easy, human frailty often turns it into 'unconscious speculation'

By WILLIAM CAI

IN THE third quarter of 2010, a slew of positive economic data was evident in the media. The idea of investing for the long term - by picking Singapore's 'solid' dividend-paying blue-chip stocks - became an attractive proposition in a low-interest-rate environment. Coincidentally, this was also when the Singapore Investor Confidence Index Poll reached a high. From a contrarian perspective, that's when one should worry.

A 'death cross' occurred when the Straits Times Index (STI) fell to 2,797. It's a term used when a security's 50-day moving average price line crosses over its 200-day moving average line from the top, generating a long-term bearish signal which suggests that investors should adjust their bullish view to bearish.

While 12 out of 18 'death crosses' resulted as false signals (whipsaws) over the past 30 years for the STI, investors should still take the bearish signal seriously. Firstly, as a lagging indicator, the signal usually occurs after the STI has fallen by 10 per cent or more, and only to be compounded by further losses if a severe bear emerges. Secondly, six out of the 18 signals resulted in losses ranging from minus 22 per cent to minus 54 per cent. Thirdly, it is worrying that more than 60 per cent of the STI constituents, which are classified as 'blue-chip' stocks, have generated the 'death cross' signal.

More importantly, the 'death cross' has also occurred for various other global markets, increasing the odds of a full-blown bear market.

The definition of an 'investment', as offered by Benjamin Graham in 1934, 'is an operation that promises the safety of principal and satisfaction of return. Operations not meeting these requirements are speculation.'

Contrary to popular belief, Warren Buffett is a great market timer. He plays the game well by raising cash when he cannot find attractively-valued stocks. He waits for opportunities to pick up stocks at fire-sale prices, especially when there's blood in the streets.

The biggest mistake an investor can make is to focus only on the idea of getting stable dividends, with disregard to price. For example, when investors buy blue chips at a high price during the mature stage of an economic cycle, this increases the possibility of seeing their stock value fall 50 per cent or more in the next economic slowdown.

Despite the potential poor risk-adjusted ratio, investors stick to the concept of buying blue-chip stocks as they harbour the hope of capital appreciation which bonds may not match. This does not make sense as corporate bonds can do the job of providing a steady income better without similar risk to equity.

Untrained investors would focus on buying blue chips with the highest reputation, quoting their good management and their ability to continue to deliver profits for the long term as reasons for investing in them. Such investors do not wish to engage in market-timing activities as they equate these to speculation. Therefore, they pay insufficient attention to prices given their assumption that well-chosen blue chips would recover from an economic downturn. Ironically, that is a speculative assumption as many of today's blue chips could become tomorrow's losers.

For example, an investor who bought SGX shares at $14.40 on Oct 2, 2007 would have seen the price fall 53 per cent as at Aug 22, 2011. Assuming dividends reinvested, the loss would be large at minus 46 per cent. Investors who bought stocks like Cosco, NOL and Yangzijiang at their peak in 2007 would still be nursing losses of between minus 50 per cent to minus 84 per cent.

Contrary to popular belief, Warren Buffett, the famous value investor, is a great market timer. He plays the game well by raising cash when he cannot find attractively-valued stocks. He waits for opportunities to pick up stocks at fire-sale prices, especially when there's blood in the streets. As the key to long-term investment success is to first avoid losing big, a true long-term investor should do the same and wait for a market crisis to buy stocks at attractive prices. Then, they can ignore the madness of short-term volatility and sell the stocks when they become overvalued. Over time, this strategy can substantially increase the wealth of investors.

For most investors, professionals included, qualitative factors like good management are difficult to deal with intelligently and such an evaluation can be clouded by an investor's own confirmation bias. Quantitative factors, like the continued ability for a business to deliver steady earnings growth, would need investors to have a considerable amount of investigation and business acumen.

Savvier investors could argue that Singapore stocks are now reasonable, based on their current price ratios and forward-looking evaluations. This requires the calculation of the intrinsic value of a business as determined by its future earnings. However, history has repeatedly shown that during the good times, many analysts become over-optimistic and assume a sustainable earnings trend. In reality, the concept of intrinsic value is arbitrary at best. It is elusive and hard to determine, due to the uncertain future and the irrational market.

In addition, few analysts dare to offer views different from the herd as it is often safer to err with the masses. For an analyst to be wrong alone, it can lead to the demise of his reputation and career. Even if the trend of earnings and intrinsic value can be determined reliably, it does not sufficiently provide a safe basis for investing, especially during a bear market.

Currently, the price-to-book (P/B) ratio for the STI stands at 1.3 times and history has also shown that since 1994, whenever the P/B ratio drops from 1.5 times, its downward momentum would bring it to lower levels. This assigns a high probability that the STI could have more to fall as it just breached its 1.5 times P/B level this month.

Unfortunately, during a mature economic cycle, undervalued blue chips are uncommon and many investors end up investing without sufficient regard to price. Investors should focus on value investing as it helps investors invest better by selecting stocks based on the margin-of-safety principle. This means that one buys undervalued stocks at a price lower than their intrinsic value.

This helps to prioritise the safety of capital while dividends are viewed as of secondary importance. While dividends come in handy as a 'cushion' to effectively lower losses when stock prices fall, dividend yields are lower when blue chips are bought at higher prices. Furthermore, during an economic downturn, companies do slash their dividend payouts to preserve cash holdings. This was true during the last crisis for blue chips like SIA, NOL, SGX, CapitaLand, DBS, UOB and ComfortDelgro, as their earnings fell.

While value-investing may seem easy, human frailty often prevents successful implementation. It is hard to prevent human emotion from corrupting an investment framework. Even if the necessary fundamental analysis is used to scan for value stocks, investors may end up with a handful of stocks from boring industries which are not what he initially deemed as blue chips. More importantly, it is hard to be fearful when others are greedy, and vice versa. It is hard to think independently and go against the herd.

Nevertheless, I hope that this article has helped instil a new level of consciousness to replace unconscious speculation. When the stock market enters a bear phase, extreme fear rather than fundamentals rules the day. Even the bluest of blue-chip value picks can fall by a considerable amount. Dividends are often insufficient to cushion a market bloodbath. How much more refuge can an expensive blue chip provide? Investors who buy stocks at a high premium during a stockmarket high unwittingly end up as 'long-term investors'.

With the current global economic slowdown, coupled with the lingering US and European sovereign debt crisis, the recent market carnage could be the beginning of something worse. Buying blue chips based on dividends alone while ignoring price, potentially deteriorating fundamentals and the economic cycle can be disastrous. It's never too late to avoid unconscious speculation and to invest wisely.

The writer is vice-president & deputy investment head at GYC Financial Advisory

Tuesday, August 23, 2011

The man whose passion is Singapore

by Teo Xuanwei 04:45 AM Aug 23, 2011

Former Deputy Prime Minister Tony Tan gave an almost embarrassed chuckle when this reporter asked whether his old Casio watch - which he has kept for over 30 years - or his battered wallet - from which he fished out S$5 for a street busker - were signs of him being sentimental or frugal.

"It works well, so I don't see any point changing it. I don't believe in changing things so long as they work. I use it until it sort of falls apart," explained Dr Tan, in his trademark matter-of-fact manner.

Dressed casually in slacks and New Balance track shoes, Dr Tan has been meeting Singaporeans from all walks of life and all races, shaking hundreds of hands a day.

Despite being stopped every few steps by Singaporeans wanting to snap a picture with him, the 71-year-old kept up a pace that this 20-something reporter found challenging to keep up with.

Dr Tan's schedule thus far has comprised four to five events each day, starting as early as 8am and ending only at 11pm after a nightly review at his campaign headquarters.

How has he managed to stay in tip-top shape amid a gruelling campaign?

His secret, he says, is his wife.

"My wife looks after me very well. She makes me a lot of chicken soup," he said.

Also his exercise regime of daily 3km jogs, swims and gym workouts is "no longer a matter of enhancement but a matter of maintenance". He added: "I don't think one can (contest the Presidential Elections) half-heartedly. Once you decide to do it, you must be prepared to cover the ground."

When asked about his passion in life, Dr Tan replied without hesitation: "Singapore."

A topic he spoke readily about at length and with passion, sharing his views on a variety of topics such as the complex challenges facing the nation, or the painstaking efforts that went into building the unique socio-political situation that the Singapore society finds itself in.

But when it came to more personal questions - including those about his family - Dr Tan was more circumspect.

"I try to keep the privacy of my family as much as possible," said Dr Tan, who has been a public figure for several decades, after he was elected as a Member of Parliament for Sembawang in 1979 in a by-election. While he retired from politics in 2006, Dr Tan remained in the public eye in his positions at Government organisations such as the National Research Foundation.

Nevertheless, Dr Tan shared with this reporter the three guiding principles of his life: Honesty, having the right motivation to do things and determination.

He said: "One has to be frank and open about what he wants to do and why he wants to do it ... When you set your mind to do something, you must have the determination to see it through."

During his Presidential candidate broadcast speech last week, Dr Tan shared that he met his wife, Mary, at university. But they could not hold their wedding dinner because of curfews imposed after the deadly riots in 1964. He added in his speech that the couple celebrated their 47th wedding anniversary this month "with our four children, their spouses and five grandchildren".

Towards the end of the interview, this reporter asked his wife what attracted her to him. At this point, Dr Tan turned to his wife and asked, with a hint of child-like nervousness: "Do you want to answer that?" They laughed a little, and then apologised, saying they had to continue their walkabout in Jurong Point shopping mall.

But as Dr Tan turned and started walking away, Mrs Tan whispered: "He's always been a gentleman."

Teo Xuanwei is a senior reporter at Today.

Former Deputy Prime Minister Tony Tan gave an almost embarrassed chuckle when this reporter asked whether his old Casio watch - which he has kept for over 30 years - or his battered wallet - from which he fished out S$5 for a street busker - were signs of him being sentimental or frugal.

"It works well, so I don't see any point changing it. I don't believe in changing things so long as they work. I use it until it sort of falls apart," explained Dr Tan, in his trademark matter-of-fact manner.

Dressed casually in slacks and New Balance track shoes, Dr Tan has been meeting Singaporeans from all walks of life and all races, shaking hundreds of hands a day.

Despite being stopped every few steps by Singaporeans wanting to snap a picture with him, the 71-year-old kept up a pace that this 20-something reporter found challenging to keep up with.

Dr Tan's schedule thus far has comprised four to five events each day, starting as early as 8am and ending only at 11pm after a nightly review at his campaign headquarters.

How has he managed to stay in tip-top shape amid a gruelling campaign?

His secret, he says, is his wife.

"My wife looks after me very well. She makes me a lot of chicken soup," he said.

Also his exercise regime of daily 3km jogs, swims and gym workouts is "no longer a matter of enhancement but a matter of maintenance". He added: "I don't think one can (contest the Presidential Elections) half-heartedly. Once you decide to do it, you must be prepared to cover the ground."

When asked about his passion in life, Dr Tan replied without hesitation: "Singapore."

A topic he spoke readily about at length and with passion, sharing his views on a variety of topics such as the complex challenges facing the nation, or the painstaking efforts that went into building the unique socio-political situation that the Singapore society finds itself in.

But when it came to more personal questions - including those about his family - Dr Tan was more circumspect.

"I try to keep the privacy of my family as much as possible," said Dr Tan, who has been a public figure for several decades, after he was elected as a Member of Parliament for Sembawang in 1979 in a by-election. While he retired from politics in 2006, Dr Tan remained in the public eye in his positions at Government organisations such as the National Research Foundation.

Nevertheless, Dr Tan shared with this reporter the three guiding principles of his life: Honesty, having the right motivation to do things and determination.

He said: "One has to be frank and open about what he wants to do and why he wants to do it ... When you set your mind to do something, you must have the determination to see it through."

During his Presidential candidate broadcast speech last week, Dr Tan shared that he met his wife, Mary, at university. But they could not hold their wedding dinner because of curfews imposed after the deadly riots in 1964. He added in his speech that the couple celebrated their 47th wedding anniversary this month "with our four children, their spouses and five grandchildren".

Towards the end of the interview, this reporter asked his wife what attracted her to him. At this point, Dr Tan turned to his wife and asked, with a hint of child-like nervousness: "Do you want to answer that?" They laughed a little, and then apologised, saying they had to continue their walkabout in Jurong Point shopping mall.

But as Dr Tan turned and started walking away, Mrs Tan whispered: "He's always been a gentleman."

Teo Xuanwei is a senior reporter at Today.

Monday, August 22, 2011

Templeton’s Mobius Sees Stock Markets Rising on Inflation

By Shani Raja and Susan Li

Aug 22, 2011 6:29 PM GMT+0800

Aug. 22 (Bloomberg) -- Mark Mobius, executive chairman of Templeton Asset Management’s emerging markets group, talks about the outlook for U.S. Federal Reserve monetary policy and global financial markets. Mobius speaks from Seoul with Susan Li on Bloomberg Television's "First Up." (Source: Bloomberg).

Global stock markets are “bouncing along the bottom” after tumbling 16 percent in the past four weeks, and will start to climb as inflation accelerates, said Templeton Asset Management’s Mark Mobius.

The U.S. Federal Reserve hasn’t given up supporting the economy by printing money and buying more Treasuries, said Mobius, executive chairman of Templeton Asset’s emerging markets group. The firm is buying commodity stocks, expecting raw material prices to rise, he said.

“At this point, I do think we’re bouncing along the bottom,” Mobius, who helps manage about $50 billion, said in a telephone interview with Bloomberg Television today. “For us in equities, it’s particularly good because people will eventually realize that to beat inflation that’s coming as a result of this higher money supply, we’re going to have to be into equities.”

The MSCI World (MXWO) Index of stocks fell last week for a fourth straight week as investors took flight after a deadlock in the U.S. congress brought the government to the brink of default, reports showed the world’s biggest economy is slowing, and concern grew that Europe’s sovereign-debt crisis will spread. The losses triggered speculation Fed Chairman Ben S. Bernanke will this weekend signal a third-round of asset purchases to help sustain a recovery.

Energy and material stocks have been among the three worst performers in the past month in the 10 industry groups tracked by the MSCI Asia-Pacific Index, as a measure of primary metals traded in London and New-York-traded oil futures slumped.

‘An Opportunity’

“It’s been an opportunity,” said Mobius. “With the amount of liquidity coming into the system, commodity prices have to be maintained at higher and higher levels. The trend is very, very clear, and that’s up.”

Mobius told Bloomberg TV Aug. 5 that he doesn’t expect the U.S. to experience a double-dip recession because of the likelihood of further economic stimulus.

The S&P 500 may stage a short-term rally because companies are cashed up and likely to buy back shares at a time when price-to-earnings ratios are low, said economist Andrew Smithers. Investors should sell shares once their holdings gain 10 percent because even after the recent rout, U.S. stocks are about 40 percent above fair value, the president of research company Smithers & Co. said in an e-mail on Aug. 18.

Standard & Poor’s 500 Index companies have about $291 in cash and short-term investments per share, according to data compiled by Bloomberg. That’s the highest since 1998, when Bloomberg data became available.

Volatility to Continue

Economists said reports this week may show U.S. companies ordered less equipment in July, and that the economy grew even less in the second quarter than previously estimated.

“It’s not certain to us what the Federal Reserve can say to calm people’s nerves,” Don Williams, chief investment officer at Platypus Asset Management Ltd. in Sydney, said in a separate Bloomberg Television interview today. “This period of volatility that we’re in has still got a way to play out.”

Global stocks will rise even amid investor concern that Europe’s sovereign debt crisis may be prolonged by German Chancellor Angela Merkel’s resistance to calls for common euro- area bonds, according to Mobius.

The region’s crisis is moving toward a resolution after European Union pledges this year to stabilize the euro-area economy and stave off a Greek default, Mobius said.

“I believe the situation in Europe will get better now that they have a facility to bail out these countries,” he said. “But in the meantime, the loss of confidence has really hit both sides of the Atlantic, and that’s something that’s going to have to wear away as we go forward.”

Mobius said today he remained interested in consumer stocks, as well as equities in emerging markets such as Brazil, China, Thailand, Indonesia and Russia. On Aug. 5, he told Bloomberg TV that emerging economies were in “better shape” than developed nations amid the turmoil roiling global markets.

Aug 22, 2011 6:29 PM GMT+0800

Aug. 22 (Bloomberg) -- Mark Mobius, executive chairman of Templeton Asset Management’s emerging markets group, talks about the outlook for U.S. Federal Reserve monetary policy and global financial markets. Mobius speaks from Seoul with Susan Li on Bloomberg Television's "First Up." (Source: Bloomberg).

Global stock markets are “bouncing along the bottom” after tumbling 16 percent in the past four weeks, and will start to climb as inflation accelerates, said Templeton Asset Management’s Mark Mobius.

The U.S. Federal Reserve hasn’t given up supporting the economy by printing money and buying more Treasuries, said Mobius, executive chairman of Templeton Asset’s emerging markets group. The firm is buying commodity stocks, expecting raw material prices to rise, he said.

“At this point, I do think we’re bouncing along the bottom,” Mobius, who helps manage about $50 billion, said in a telephone interview with Bloomberg Television today. “For us in equities, it’s particularly good because people will eventually realize that to beat inflation that’s coming as a result of this higher money supply, we’re going to have to be into equities.”

The MSCI World (MXWO) Index of stocks fell last week for a fourth straight week as investors took flight after a deadlock in the U.S. congress brought the government to the brink of default, reports showed the world’s biggest economy is slowing, and concern grew that Europe’s sovereign-debt crisis will spread. The losses triggered speculation Fed Chairman Ben S. Bernanke will this weekend signal a third-round of asset purchases to help sustain a recovery.

Energy and material stocks have been among the three worst performers in the past month in the 10 industry groups tracked by the MSCI Asia-Pacific Index, as a measure of primary metals traded in London and New-York-traded oil futures slumped.

‘An Opportunity’

“It’s been an opportunity,” said Mobius. “With the amount of liquidity coming into the system, commodity prices have to be maintained at higher and higher levels. The trend is very, very clear, and that’s up.”

Mobius told Bloomberg TV Aug. 5 that he doesn’t expect the U.S. to experience a double-dip recession because of the likelihood of further economic stimulus.

The S&P 500 may stage a short-term rally because companies are cashed up and likely to buy back shares at a time when price-to-earnings ratios are low, said economist Andrew Smithers. Investors should sell shares once their holdings gain 10 percent because even after the recent rout, U.S. stocks are about 40 percent above fair value, the president of research company Smithers & Co. said in an e-mail on Aug. 18.

Standard & Poor’s 500 Index companies have about $291 in cash and short-term investments per share, according to data compiled by Bloomberg. That’s the highest since 1998, when Bloomberg data became available.

Volatility to Continue

Economists said reports this week may show U.S. companies ordered less equipment in July, and that the economy grew even less in the second quarter than previously estimated.

“It’s not certain to us what the Federal Reserve can say to calm people’s nerves,” Don Williams, chief investment officer at Platypus Asset Management Ltd. in Sydney, said in a separate Bloomberg Television interview today. “This period of volatility that we’re in has still got a way to play out.”

Global stocks will rise even amid investor concern that Europe’s sovereign debt crisis may be prolonged by German Chancellor Angela Merkel’s resistance to calls for common euro- area bonds, according to Mobius.

The region’s crisis is moving toward a resolution after European Union pledges this year to stabilize the euro-area economy and stave off a Greek default, Mobius said.

“I believe the situation in Europe will get better now that they have a facility to bail out these countries,” he said. “But in the meantime, the loss of confidence has really hit both sides of the Atlantic, and that’s something that’s going to have to wear away as we go forward.”

Mobius said today he remained interested in consumer stocks, as well as equities in emerging markets such as Brazil, China, Thailand, Indonesia and Russia. On Aug. 5, he told Bloomberg TV that emerging economies were in “better shape” than developed nations amid the turmoil roiling global markets.

Saturday, August 20, 2011

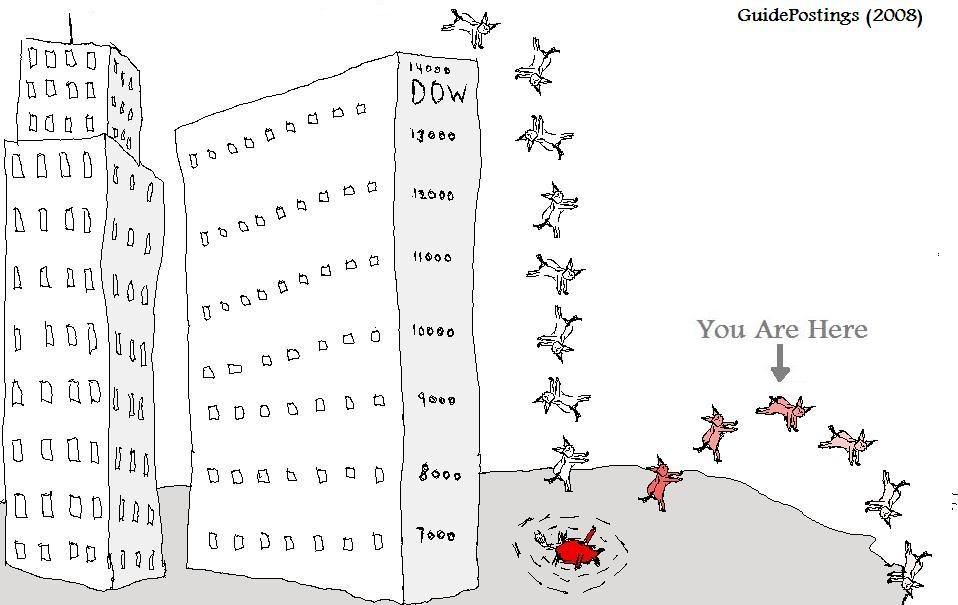

The great market panic

Wealth

Published August 20, 2011

INVESTING

The recent slump in global share prices reflects fears of a recession in the US and Europe, and worries that this will drag down the rest of the world. Are these fears justified?

By SHANE OLIVER

AMP CAPITAL INVESTORS

'I have observed that not the man who hopes when others despair, but the man who despairs when others hope, is admired by a large class of persons as a sage.'

J S Mill